The taxation landscape of Sovereign Gold Bond (SGB) has witnessed a significant shift pursuant to amendments proposed in the Union Budget 2026, effective from 1 April 2026 (FY 2026-27).

SGBs have traditionally been a tax-efficient mode of investing in gold. However, the latest amendment restricts the capital gains exemption benefit, thereby altering post-tax return calculations for certain investors.

This article provides a comparative understanding of the taxation regime before and after the amendment.

Taxation of SGBs – Position Before Budget 2026

Taxation of SGBs – Position Before Budget 2026

A. Capital Gains at Maturity (8 Years)

Prior to the amendment:

Capital gains on redemption at maturity were fully exempt from tax.

This exemption applied irrespective of whether the bonds were purchased in the primary issue or through the secondary market.

This made SGBs highly attractive even for secondary market investors.

B. Sale Before Maturity (Through Stock Exchange)

If sold before maturity:

Held up to 12 months → Short-Term Capital Gain (STCG) taxed at applicable slab rate.

Held for more than 12 months → Long-Term Capital Gain (LTCG) taxed at 12.5% without indexation.

C. Interest Income

The 2.5% annual interest continues to be taxable under the head “Income from Other Sources.”

Taxation of SGBs – After Budget 2026 (Effective 1 April 2026)

Taxation of SGBs – After Budget 2026 (Effective 1 April 2026)

The amendment significantly narrows the scope of exemption.

Key Change Introduced

Key Change Introduced

Capital gains exemption at maturity will now be available only if:

The investor subscribed to the SGB at the original issue price (primary issuance), and

The investor subscribed to the SGB at the original issue price (primary issuance), and

The bond is held continuously until maturity.

What Becomes Taxable?

In the following cases, capital gains will now be taxable:

A. SGBs purchased from the secondary market (even if held till maturity)

B. Bonds originally subscribed but sold before maturity

C. Any transfer prior to maturity

Applicable Tax Rates

STCG (≤ 12 months) → Slab rate

LTCG (> 12 months) → 12.5% without indexation

D. Interest taxation remains unchanged.

Comparative Summary

Comparative Summary

Scenario Before Budget 2026 After Budget 2026Original subscriber, held till maturity ExemptSecondary market buyer, held till maturity Exempt TaxableSale before maturity Taxable Interest income Taxable.

Practical Implications for Investors

Practical Implications for Investors

A. Secondary market investors lose the tax-free maturity advantage.

B. Post-tax returns must now be recalculated before investing in SGBs from the exchange.

C. Long-term investors subscribing at primary issuance continue to enjoy the tax exemption.

D. Portfolio exit strategy planning becomes crucial for existing secondary market holders before 1 April 2026.

5️⃣ Conclusion

The amendment aims to restrict the tax benefit to genuine long-term original subscribers and prevent tax arbitrage via secondary market purchases.

While SGBs remain a compelling gold investment instrument, the tax efficiency element has now become selective rather than universal.

Investors are advised to evaluate:

A. Purchase mode (primary vs secondary)

B. Holding period

C. Expected capital appreciation

D. Post-tax return impact

The Taxation landscape of Sovereign Gold Bond (SGB) has witnessed a significant shift pursuant to amendments proposed in the Union Budget 2026, effective from 1 April 2026 (FY 2026-27). SGBs have...

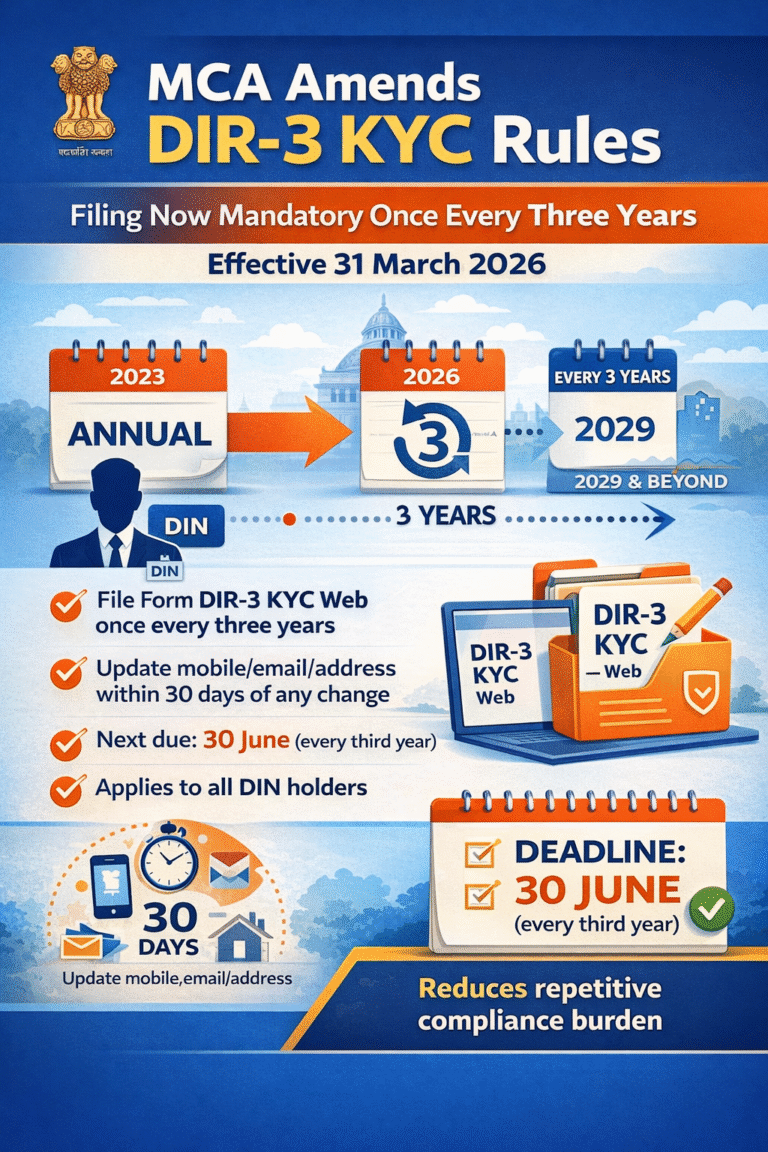

The Ministry of Corporate Affairs (MCA) has notified a significant amendment to the Companies (Appointment and Qualification of Directors) Rules, 2014, bringing major relief to directors across India...

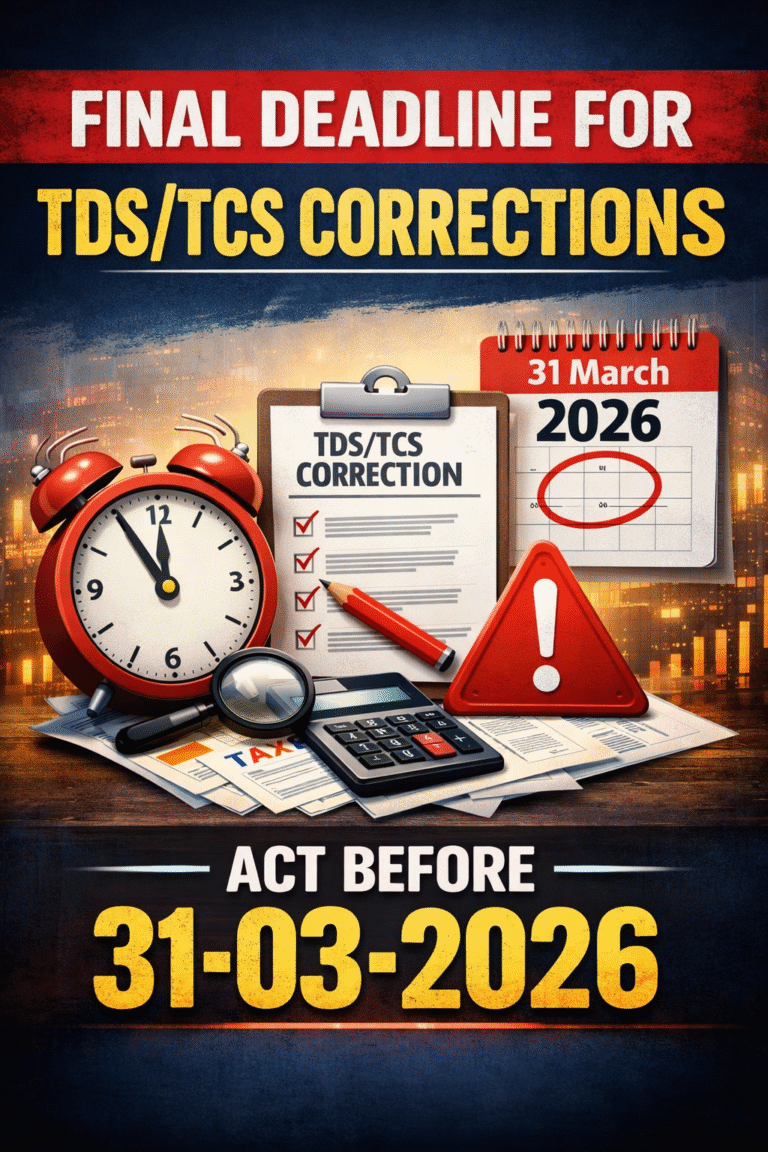

Final Deadline for TDS/TCS Corrections – Act Before 31-03-2026 The Income-tax compliance landscape is undergoing a significant transition. A crucial deadline is approaching that every deductor and...

ESOP Taxation -Perquisite to Capital Gain...

📌 1. What is Section 194T?

Section 194T is a new TDS provision inserted by the Finance (No. 2) Act, 2024, effective from 1 April 2025. It requires a partnership firm or LLP to deduct tax at source on...

Missed the ITR filing deadline for AY 2025-26? Do not panic. Learn your options, penalties, and step-by-step solutions to stay compliant and avoid heavy fines...

Learn about the most common mistakes made during GST registration in India and how to avoid them for a smooth process...

The Taxation landscape of Sovereign Gold Bond (SGB) has witnessed a significant shift pursuant to...

The Ministry of Corporate Affairs (MCA) has notified a significant amendment to the Companies...

Final Deadline for TDS/TCS Corrections – Act Before 31-03-2026 The Income-tax compliance landscape...

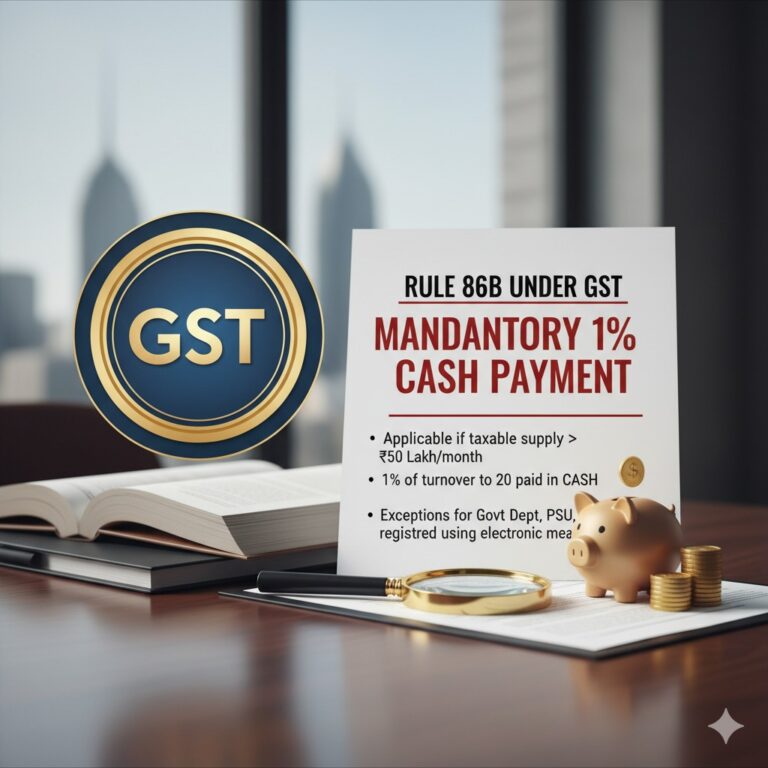

Rule 86B Under GST...

Baggage Rules,2026...

ESOP Taxation -Perquisite to Capital Gain...

📌 1. What is Section 194T?

Section 194T is a new TDS provision inserted by the Finance (No. 2) Act...

Missed the ITR filing deadline for AY 2025-26? Do not panic. Learn your options, penalties, and...

Learn about the most common mistakes made during GST registration in India and how to avoid them for...