🔎What Has Changed?

Earlier, buyback taxation operated under a different framework where the tax incidence was primarily at the company level. However, under the proposed amendment:

Buyback proceeds will now be taxed as Capital Gains in the hands of all shareholders.

In addition, to discourage misuse by promoters, an additional buyback tax has been introduced specifically for promoters.

Effective Tax Impact

Effective Tax Impact

The revised structure results in the following effective tax rates:

Corporate Promoters: 22% effective tax

Non-Corporate Promoters: 30% effective tax

This ensures that promoters—who typically have significant control over buyback decisions—bear a higher and more equitable tax burden where buybacks are used as a tax planning tool.

Objective Behind the Amendment

Objective Behind the Amendment

The government’s intent appears twofold:

•Prevent Tax Arbitrage: Promoters were, in certain cases, structuring buybacks in a manner that resulted in lower tax outgo compared to dividends or other distribution mechanisms.

• Shift to Shareholder-Level Taxation: Aligning buyback taxation with capital gains principles enhances neutrality and reduces distortions between different modes of profit distribution.

Broader Implications

Broader Implications

• Companies may reassess whether buybacks remain an efficient method of returning surplus to shareholders.

• Promoters will need to factor in the additional tax cost before opting for buybacks.

• Minority shareholders will now directly evaluate capital gains implications based on their holding period and tax profile.

Conclusion

Conclusion

The amendment marks a clear policy stance against the misuse of buyback provisions for tax planning. By taxing buybacks as capital gains for all shareholders and imposing an additional tax burden on promoters, the Budget seeks to balance flexibility in capital restructuring with fiscal prudence and fairness.

As the new provisions come into effect, both companies and promoters must revisit their capital allocation strategies to ensure tax efficiency while remaining compliant with the evolving regulatory landscape.

📢 The Union Budget 2026 has introduced a significant shift in the taxation of share buybacks with the objective of curbing improper use of buyback mechanisms by promoters. The amendment aims to bring...

The Taxation landscape of Sovereign Gold Bond (SGB) has witnessed a significant shift pursuant to amendments proposed in the Union Budget 2026, effective from 1 April 2026 (FY 2026-27). SGBs have...

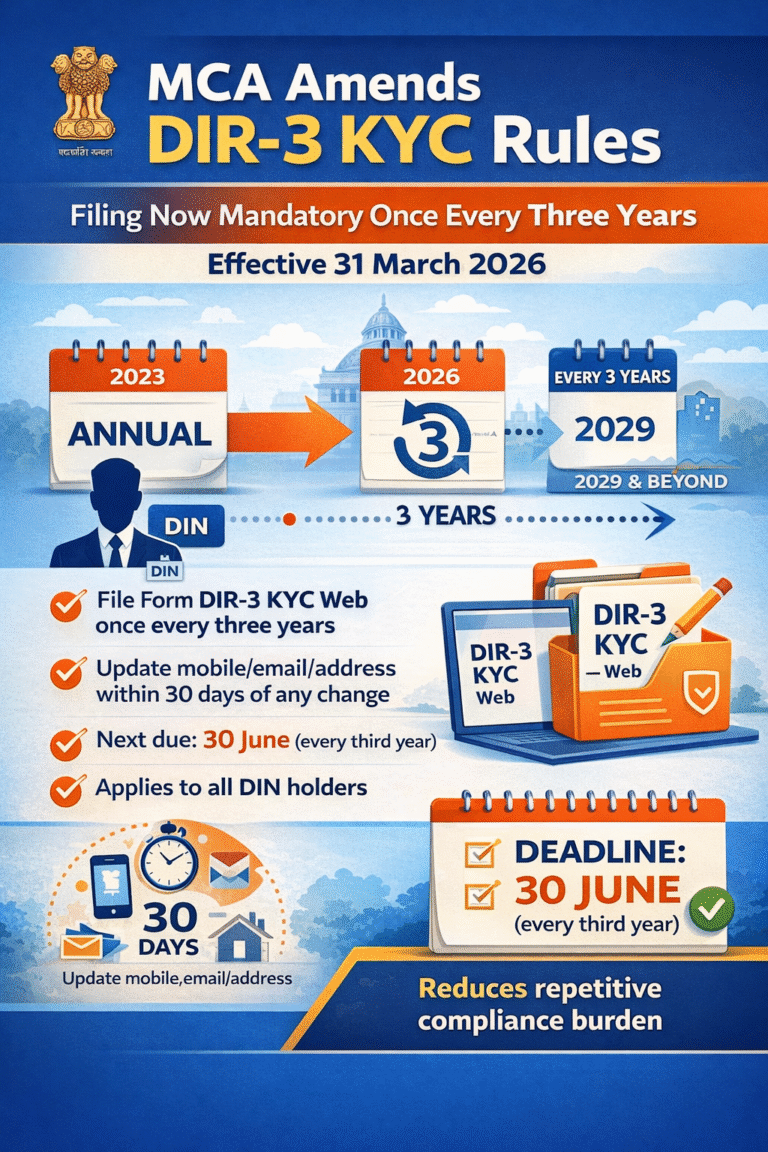

The Ministry of Corporate Affairs (MCA) has notified a significant amendment to the Companies (Appointment and Qualification of Directors) Rules, 2014, bringing major relief to directors across India...

Final Deadline for TDS/TCS Corrections – Act Before 31-03-2026 The Income-tax compliance landscape is undergoing a significant transition. A crucial deadline is approaching that every deductor and...

ESOP Taxation -Perquisite to Capital Gain...

📌 1. What is Section 194T?

Section 194T is a new TDS provision inserted by the Finance (No. 2) Act, 2024, effective from 1 April 2025. It requires a partnership firm or LLP to deduct tax at source on...

Missed the ITR filing deadline for AY 2025-26? Do not panic. Learn your options, penalties, and step-by-step solutions to stay compliant and avoid heavy fines...

📢 The Union Budget 2026 has introduced a significant shift in the taxation of share buybacks with...

The Taxation landscape of Sovereign Gold Bond (SGB) has witnessed a significant shift pursuant to...

The Ministry of Corporate Affairs (MCA) has notified a significant amendment to the Companies...

Final Deadline for TDS/TCS Corrections – Act Before 31-03-2026 The Income-tax compliance landscape...

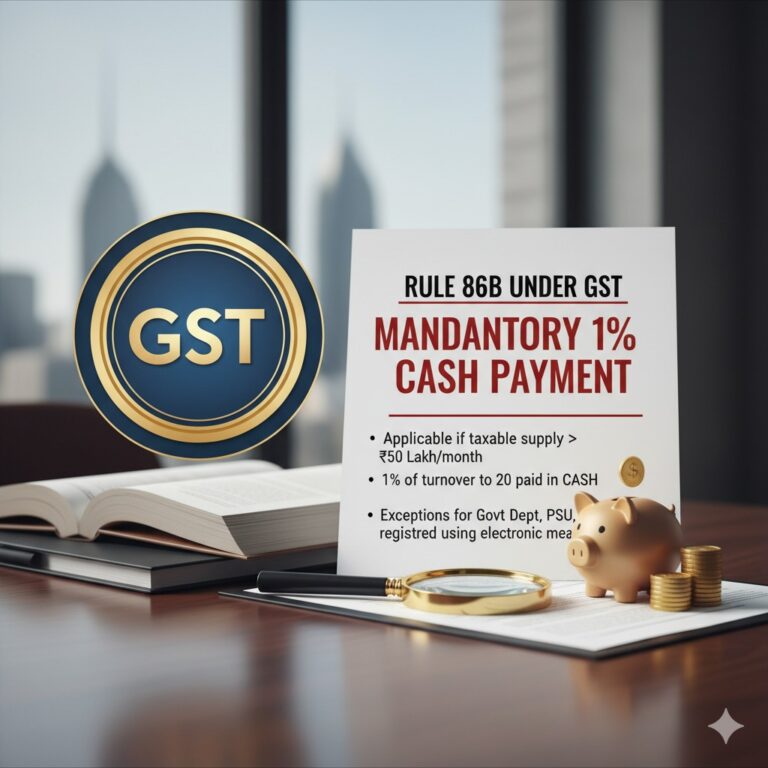

Rule 86B Under GST...

Baggage Rules,2026...

ESOP Taxation -Perquisite to Capital Gain...

📌 1. What is Section 194T?

Section 194T is a new TDS provision inserted by the Finance (No. 2) Act...

Missed the ITR filing deadline for AY 2025-26? Do not panic. Learn your options, penalties, and...