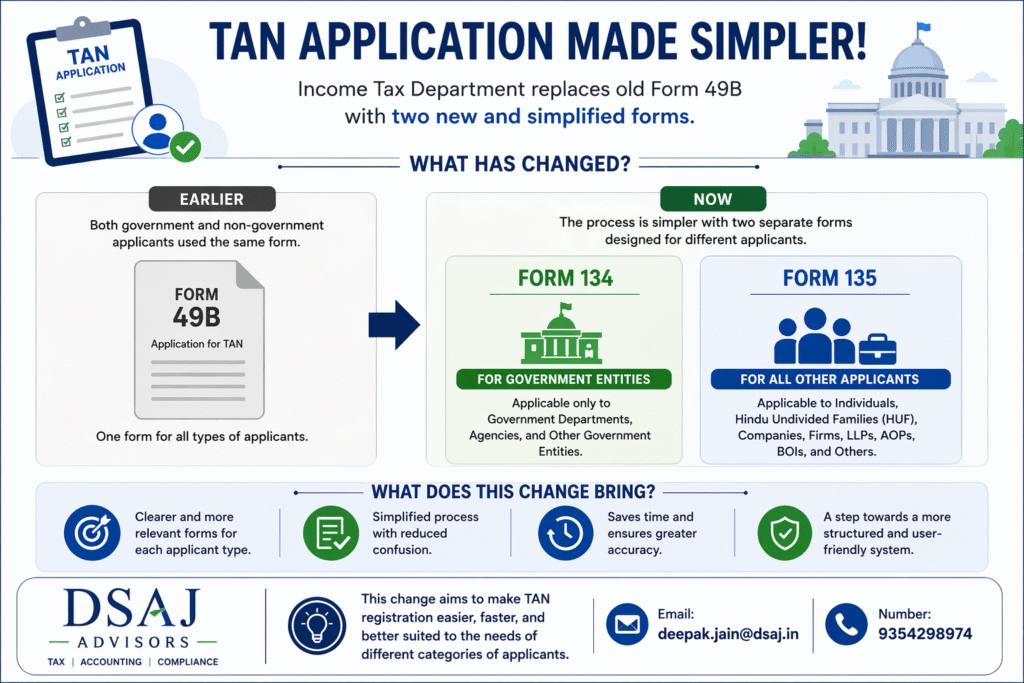

The Income Tax Department has introduced Form No. 134 and Form No. 135 for the allotment of Tax Deduction and Collection Account Number (TAN), replacing the existing Form 49B. These changes aim to simplify the application process and improve compliance through better documentation and categorization.

Let’s understand the new forms in detail.

🔍 What is TAN and Why is it Required?

TAN (Tax Deduction and Collection Account Number) is a unique 10-digit alphanumeric number required for:

A. Deducting Tax at Source (TDS)

B. Collecting Tax at Source (TCS)

C. Filing TDS/TCS returns

D. Issuing TDS/TCS certificates

Any person or entity responsible for TDS/TCS compliance must obtain TAN.

↗️ Introduction of Form 134 & 135

The earlier Form 49B has now been replaced with two separate forms:

Form No. | Applicable To |

|---|---|

Form 134 | Government entities |

Form 135 | Non-Government entities (Individuals, Companies, LLPs, etc.) |