1. What is Partner’s Remuneration?

Partner’s remuneration refers to:

-

Salary

-

Bonus

-

Commission

-

Any other payment of similar nature

paid by a partnership firm or LLP to its partners, as authorised by the partnership deed.

2. Existing Tax Treatment (Up to 31 March 2026) In the Hands of the Firm

In the Hands of the Firm

-

Allowed as a deduction under Section 40(b), subject to limits.

-

No TDS was required on such payments.

In the Hands of the Partner

-

Taxable as Business Income.

-

Partner pays advance tax / self-assessment tax as applicable.

Key Point:

Key Point:

Until now, partner remuneration was outside the scope of TDS, as partners are not considered “employees” of the firm.

3. Introduction of Section 194T – A Game Changer

To widen the tax base and improve reporting, the Finance Act has introduced Section 194T. Effective Date

Effective Date Applicable from 1 April 2026

Applicable from 1 April 2026

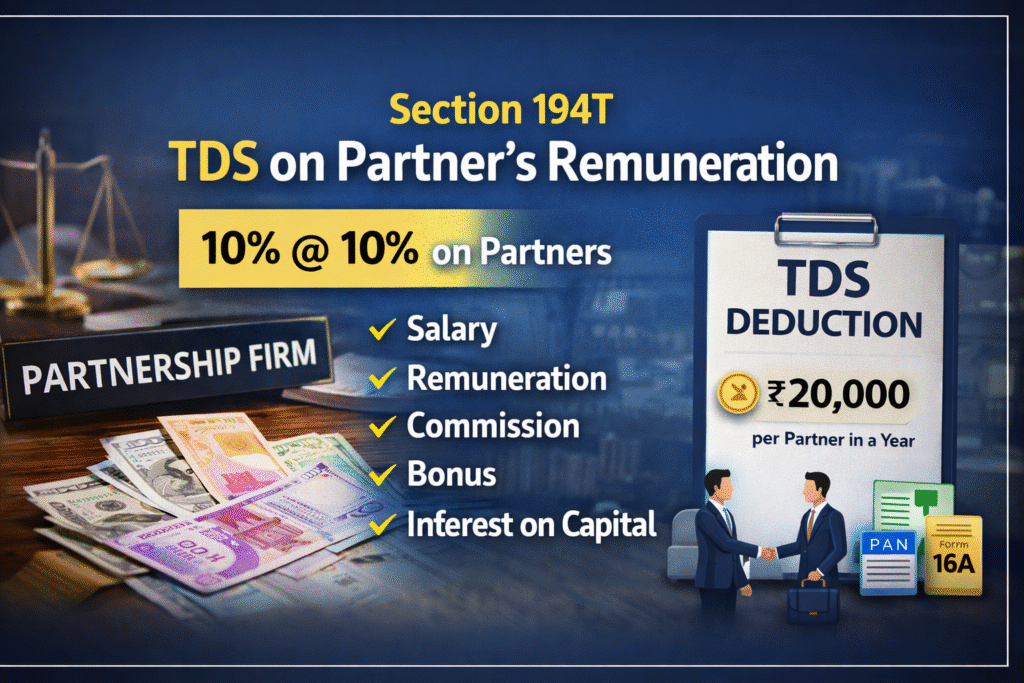

4. Key Provisions of Section 194T

| Particulars | Details |

|---|---|

| Applicable To | Partnership Firms & LLPs |

| Nature of Payment | Remuneration, salary, bonus, commission, interest |

| Recipient | Resident Partner |

| TDS Rate | 10% |

| Threshold Limit | ₹20,000 per partner per financial year |

| Time of Deduction | At credit or payment, whichever is earlier |

5. Payments Covered Under Section 194T

TDS will apply on:

-

Partner’s salary or remuneration

-

Bonus or commission

-

Interest on capital

-

Any other payment of similar nature

Even if the amount is disallowed under Section 40(b), TDS obligation will still arise.

Even if the amount is disallowed under Section 40(b), TDS obligation will still arise.

6. Practical Impact on Firms & LLPs

For Firms:

-

Mandatory TDS compliance

-

Quarterly TDS returns to be filed

-

Issuance of TDS certificates to partners

-

Increased compliance cost

For Partners:

-

TDS credit available in Form 26AS

-

Reduced advance tax burden

-

Better tax tracking and transparency

7. Action Points for Taxpayers Review partnership deeds Update accounting & payroll systems Plan cash flows considering TDS deduction Educate partners about reduced net receipts

Review partnership deeds Update accounting & payroll systems Plan cash flows considering TDS deduction Educate partners about reduced net receipts