What is Rule 86B?

Rule 86B restricts the utilisation of ITC for payment of output GST liability beyond 99% in certain cases.

In simple terms:

A taxpayer cannot use ITC to discharge more than 99% of output GST liability.

At least 1% of the output tax liability must be paid in cash through the Electronic Cash Ledger.This restriction applies on a monthly basis, subject to prescribed conditions.

When Does Rule 86B Apply?

Rule 86B becomes applicable when:

The value of taxable outward supplies (excluding exempt and zero-rated supplies) exceeds ₹50 lakh in a month, and

The taxpayer is discharging output tax liability using the Electronic Credit Ledger.

If both conditions are satisfied, a minimum 1% of output tax liability must be paid in cash, irrespective of the ITC balance available.

Illustration

Assume:

Taxable outward supplies in a month: ₹75 lakh

Output GST liability: ₹13,50,000

ITC available: ₹20 lakh

Maximum ITC that can be utilised:

99% of ₹13,50,000 = ₹13,36,500

Minimum cash payment required:

1% of ₹13,50,000 = ₹13,500

Even though ITC is sufficient, ₹13,500 must mandatorily be paid in cash.

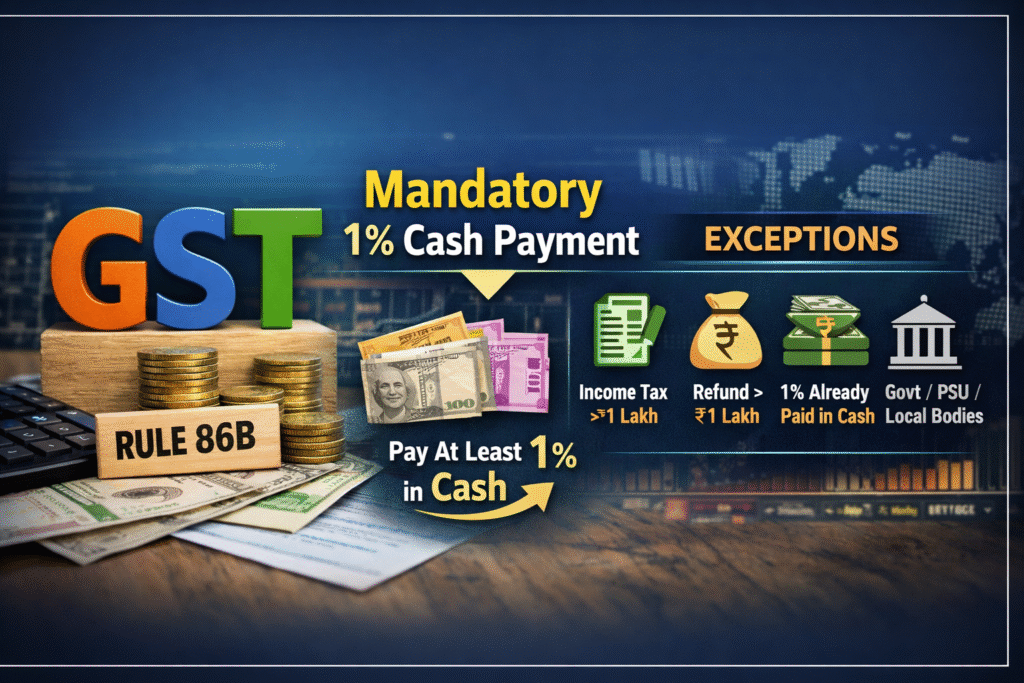

Exceptions to Rule 86B – When Restriction Does Not Apply

The restriction under Rule 86B shall not apply if any one of the following conditions is satisfied:

1. Income Tax Payment Criteria

Where any of the following persons have paid income tax exceeding ₹1 lakh in each of the last two financial years, for which the due date to file return under Section 139(1) of the Income Tax Act, 1961 has expired:

The registered person; or

The proprietor, karta, or Managing Director of the registered person; or

Any of the partners, whole-time directors, or such other person, as applicable.

2.Refund on Exports or Inverted Duty Structure

Where the registered person has received a refund exceeding ₹1 lakh in the preceding financial year on account of:

Exports made under Letter of Undertaking (LUT); or

Refund due to inverted duty structure.

3.Cumulative Cash Payment Condition

Where the registered person has discharged output tax liability through the Electronic Cash Ledger in excess of 1% of total output tax liability cumulatively up to the said month in the current financial year.

If the 1% threshold is already satisfied cumulatively, the restriction will not apply for subsequent months.

4.Specified Government Entities

Where the registered person is:a) Government Department

b) Public Sector Undertaking (PSU)

c) Local Authority

d) Statutory AuthorityImportant Clarification

Satisfaction of any one of the above conditions is sufficient for non-applicability of Rule 86B.

Taxpayers should evaluate these exemptions at the beginning of each financial year and maintain adequate documentation to support eligibility in case of scrutiny.

3. Why Was Rule 86B Introduced?

Rule 86B was introduced to:

a) Curb fake ITC claims and fraudulent invoicing

b) Prevent circular trading transactions

c) Ensure minimum cash flow to the Government

d) Strengthen compliance oversight for high-turnover entities

d) The primary objective is to restrict misuse of ITC by suspicious or non-compliant taxpayers.

e) Practical Impact on Businesses

For genuine businesses, Rule 86B impacts:

a) Working capital management

b) ITC utilisation planning

c) Monthly GST compliance strategy

d) Cash flow forecasting

Non-compliance may result in:

a) Incorrect GSTR-3B filing

b) Interest liability

c) GST notices

d) Departmental scrutiny

Compliance Checklist

Monitor monthly taxable turnover (₹50 lakh threshold) Evaluate income tax payment eligibility annually Track cumulative 1% cash payment ratio Maintain supporting documents for exemption claims Review ITC utilisation before filing GSTR-3B

Monitor monthly taxable turnover (₹50 lakh threshold) Evaluate income tax payment eligibility annually Track cumulative 1% cash payment ratio Maintain supporting documents for exemption claims Review ITC utilisation before filing GSTR-3BConclusion

Rule 86B is a compliance control mechanism aimed at preventing misuse of ITC while ensuring minimum cash contribution by high-turnover taxpayers. While genuine businesses may qualify for exemptions, periodic evaluation and proper compliance monitoring are essential to avoid litigation and penalties.

Share on

Facebook

Twitter

LinkedIn