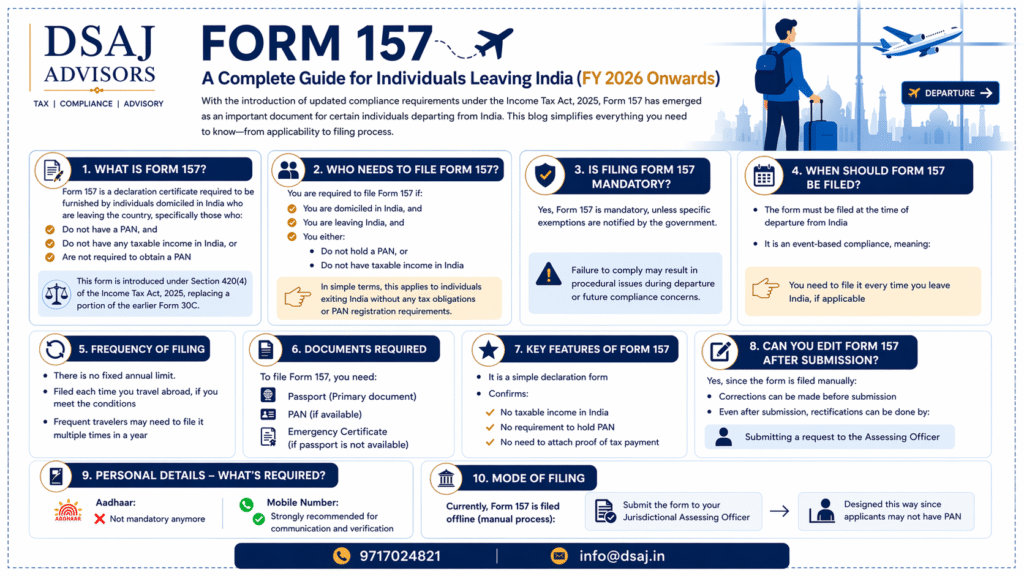

With the introduction of updated compliance requirements under the Income Tax Act, 2025, Form 157 has emerged as an important document for certain individuals departing from India. This blog simplifies everything you need to know—from applicability to filing process.

📌 What is Form 157?

Form 157 is a declaration certificate required to be furnished by individuals domiciled in India who are leaving the country, specifically those who:

Do not have a PAN, and

Do not have any taxable income in India, or

Are not required to obtain a PAN

This form is introduced under Section 420(4) of the Income Tax Act, 2025, replacing a portion of the earlier Form 30C.

👤 Who Needs to File Form 157?

You are required to file Form 157 if:

You are domiciled in India, and

You are leaving India, and

You either:

Do not hold a PAN, or

Do not have taxable income in India

👉 In simple terms, this applies to individuals exiting India without any tax obligations or PAN registration requirements.

⚖️ Is Filing Form 157 Mandatory?

Yes, Form 157 is mandatory, unless specific exemptions are notified by the government.

Failure to comply may result in procedural issues during departure or future compliance concerns.

⏳ When Should Form 157 Be Filed?

The form must be filed at the time of departure from India

It is an event-based compliance, meaning:

👉 You need to file it every time you leave India, if applicable

🔁 Frequency of Filing

There is no fixed annual limit.

Filed each time you travel abroad, if you meet the conditions

Frequent travelers may need to file it multiple times in a year

📄 Documents Required

To file Form 157, you need:

• Passport (Primary document)

• PAN (if available)

• Emergency Certificate (if passport is not available)

✍️ Key Features of Form 157

It is a simple declaration form

Confirms:

• No taxable income in India

• No requirement to hold PAN

• No need to attach proof of tax payment