The provisions relating to Tax Collected at Source (TCS) on overseas tour program packages under the Income-tax Act, 1961 have been rationalised to introduce a uniform rate of 2%.

With effect from 1st April 2026, the earlier multi-rate structure under Section 206C(1G) stands replaced by a simplified regime, aimed at reducing compliance burden and easing liquidity constraints for taxpayers.

📜 1. Legal Framework – Section 206C(1G)

Section 206C(1G) governs the collection of TCS in respect of:

Overseas tour program packages, and

Remittances under the Liberalised Remittance Scheme (LRS)

As per the Explanation to the section, an “overseas tour program package” includes:

Any package offering visit to a country or countries outside India and includes expenses for travel, hotel stay, boarding, lodging or any other expenditure of a similar nature.

The obligation to collect TCS lies with:

The seller of such package (i.e., tour operator)

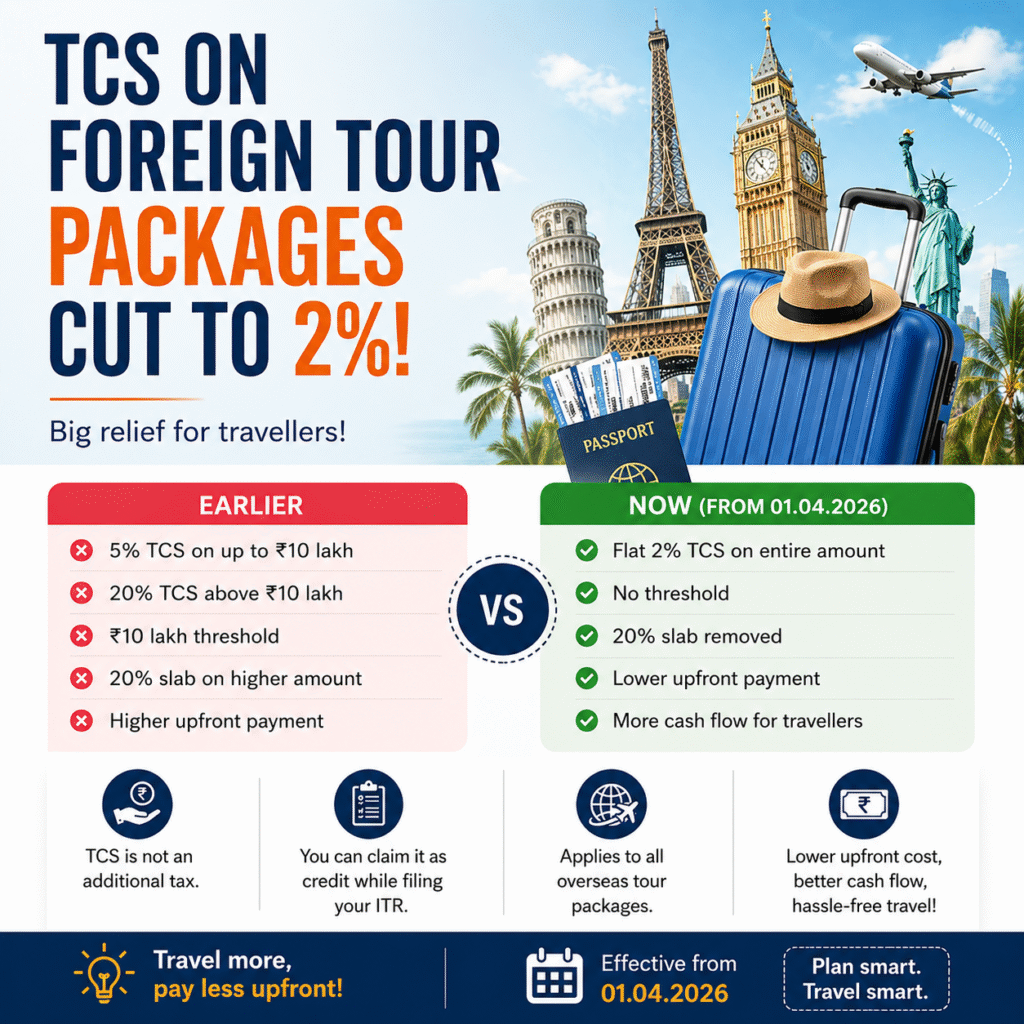

🔄 2. Earlier Position (Up to 31.03.2026)

Prior to the revised provisions, the TCS structure was:

5% TCS on consideration up to ₹10,00,000

20% TCS on consideration exceeding ₹10,00,000

This resulted in a higher upfront tax burden, especially in case of high-value international travel.

⚖️ 3. Revised Provisions (w.e.f. 01.04.2026)

The amended framework provides:

✅ Flat 2% TCS Rate

A uniform rate of 2% on the entire consideration for overseas tour packages

❌ Removal of Threshold

The earlier threshold of ₹10,00,000 is no longer applicable

❌ Elimination of Higher Rate

The 20% TCS rate on higher-value packages has been withdrawn

📊 4. Comparative Position

Particulars Earlier Provision Revised Provision

Applicable Section 206C(1G) 206C(1G)

TCS Rate 5% / 20% 2% (Flat)

Threshold Limit ₹10,00,000 ❌ Not Applicable

Higher Rate 20% ❌ Removed

💡 5. Illustrative Impact

Consideration for overseas tour package: ₹15,00,000

🔴 Earlier:

₹10,00,000 @ 5% = ₹50,000

₹5,00,000 @ 20% = ₹1,00,000

👉 Total TCS = ₹1,50,000

🟢 Now:

₹15,00,000 @ 2% = ₹30,000

👉 Reduction in upfront TCS outflow: ₹1,20,000

🧾 6. Nature of TCS – Legal Clarification

It is important to note:

TCS is not an additional tax liability, but

A mechanism for collection of tax at source

As per Section 199 read with Rule 37-I:

TCS collected is treated as tax paid on behalf of the buyer

Credit can be claimed while filing the return of income

🏢 7. Compliance Obligations for Tour Operators

The seller is required to:

Collect TCS at the time of receipt or booking, whichever is earlier

Deposit TCS within prescribed timelines (as per Rule 37CA)

File quarterly TCS returns in Form 27EQ

Issue TCS certificate (Form 27D)

👥 8. Implications for Taxpayers

💰 Improved Liquidity

Significant reduction in upfront tax burden

📉 Simplified Compliance

No need to track thresholds

🌍 Encouragement to Overseas Travel

Reduced cost barrier for international trips

🔄 9. Related Aspect – LRS Transactions

TCS provisions under Section 206C(1G) also apply to remittances under the Liberalised Remittance Scheme (LRS), including:

Education

Medical purposes

The rationalised approach reflects a move towards uniformity and ease of compliance.

🧠 10. Professional Commentary

The shift to a flat 2% TCS rate represents a move towards:

Simplification of tax provisions

Reduction in taxpayer hardship

Better compliance efficiency

The earlier structure, though effective for tracking high-value foreign expenditure, led to:

Cash flow blockage

Increased administrative complexity

The revised framework strikes a balance between tax monitoring and taxpayer convenience.

📌 Conclusion

The rationalisation of TCS under Section 206C(1G) marks a significant step towards a simpler and more taxpayer-friendly regime.

✔️ Lower upfront financial burden

✔️ Streamlined compliance

✔️ Positive impact on travel and allied sectors