Legal Framework Governing GST Notices

Legal Framework Governing GST Notices

GST notices are issued under the Central Goods and Services Tax Act, 2017 (CGST Act) and related rules. The most commonly invoked provisions include:

Section 46 – Notice for non-filing of returns (GSTR-3A)

Section 61 – Scrutiny of returns (ASMT-10)

Section 65 – Audit by tax authorities

Section 66 – Special audit

Section 67 – Inspection, search & seizure

Section 73 – Demand (non-fraud cases)

Section 74 – Demand (fraud/suppression cases)

Section 50 – Interest on delayed payment

Section 122 – Penalty provisions

Key Insight: The section under which notice is issued determines the defense strategy, documentation requirement, and timeline.

Key Insight: The section under which notice is issued determines the defense strategy, documentation requirement, and timeline.

Types of GST Notices & Prescribed Forms

Types of GST Notices & Prescribed Forms

| Notice Type | Form | Section | Purpose |

|---|---|---|---|

| Non-filing of returns | GSTR-3A | Sec 46 | Filing compliance |

| Scrutiny notice | ASMT-10 | Sec 61 | Mismatch/variance |

| Demand (non-fraud) | DRC-01 | Sec 73 | Tax short paid |

| Demand (fraud cases) | DRC-01 | Sec 74 | Fraud/suppression |

| Registration clarification | REG-03 | Rule 9 | Query resolution |

| Final demand order | DRC-07 | Sec 73/74 | Adjudication |

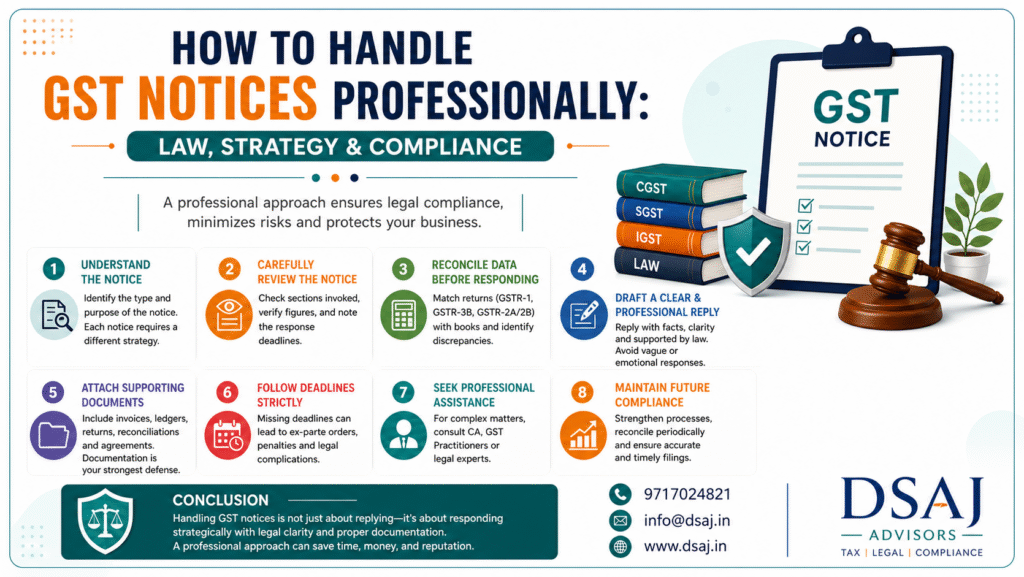

Step 1: Preliminary Evaluation of NoticeImmediately upon receipt:

Step 1: Preliminary Evaluation of NoticeImmediately upon receipt:

Verify DIN (Document Identification Number)

Verify DIN (Document Identification Number)

Check jurisdiction & issuing authority

Identify section & allegations

Note response deadline (7–30 days typically)

Important: Failure to respond may result in ex-parte orders under Section 73/74.

Important: Failure to respond may result in ex-parte orders under Section 73/74.

Step 2: Documentation & ReconciliationA strong reply is backed by accurate data and reconciliation.

Step 2: Documentation & ReconciliationA strong reply is backed by accurate data and reconciliation.

Key Documents Required:

Key Documents Required:

- GST Returns: GSTR-1, GSTR-3B

- Auto statements: GSTR-2A / 2B

- Books of accounts & trial balance

- Tax invoices & supporting documents

- E-way bills (if applicable)

Critical Reconciliations:

Critical Reconciliations:

- GSTR-1 vs GSTR-3B

- GSTR-2B vs ITC claimed

- Books vs GST returns

Step 3: Drafting a Legally Sustainable Reply

Step 3: Drafting a Legally Sustainable Reply Suggested Structure:

Suggested Structure: Step 4: Filing Reply on GST Portal

Step 4: Filing Reply on GST Portal Login to GST Portal

Login to GST Portal Step 5: Voluntary Payment – Legal Benefits

Step 5: Voluntary Payment – Legal Benefits Step 6: Personal Hearing & Adjudication

Step 6: Personal Hearing & Adjudication Ex-parte orders

Ex-parte orders Ignoring deadlines

Ignoring deadlines Conclusion

Conclusion