Filing the correct Income Tax Return (ITR) form is one of the most important compliance requirements for taxpayers in India. Choosing the wrong form may lead to defective return notices, delays in processing refunds, or unnecessary scrutiny from the Income Tax Department.

For the Financial Year 2025-26 corresponding to Assessment Year 2026-27, taxpayers must carefully determine the applicable ITR form based on the nature of income, taxpayer category, and applicable provisions under the Income-tax Act, 1961.

This article provides a detailed overview of the various ITR forms, eligibility criteria, and important due dates for FY 2025-26.

🧾 What is an ITR Form?

An Income Tax Return (ITR) form is the prescribed format through which taxpayers report their income, deductions, taxes paid, and other financial information to the Income Tax Department.

Different ITR forms are notified for different categories of taxpayers such as:

• Salaried Individuals

• Business Owners

• Professionals

• Companies

• LLPs

• Trusts

• NGOs

• Partnership Firms

Selecting the correct form depends on:

✅ Nature of Income

✅ Residential Status

✅ Turnover / Income Threshold

✅ Type of Entity

✅ Capital Gains or Foreign Assets

✅ Presumptive Taxation Scheme Applicability

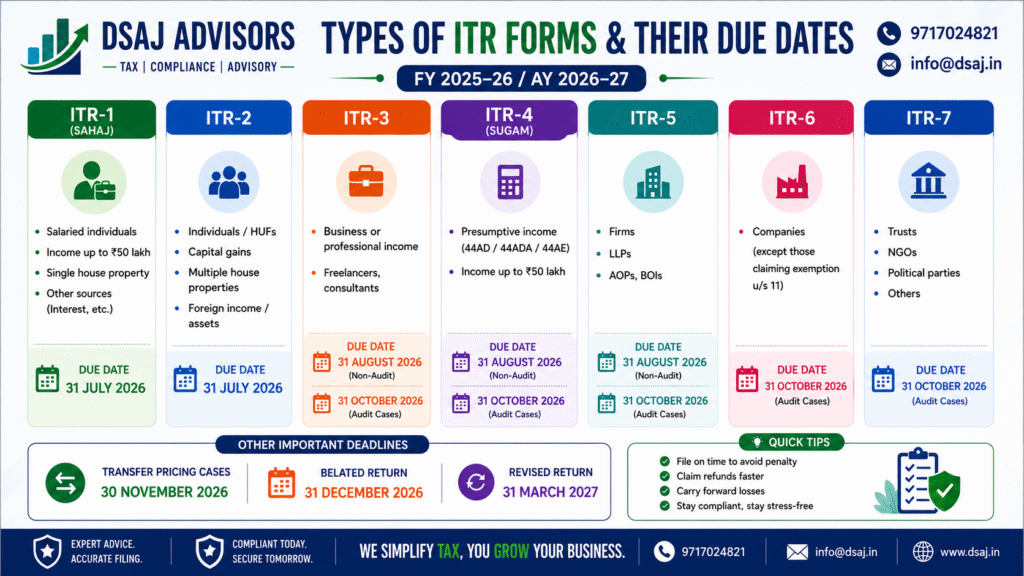

📌 Types of ITR Forms for FY 2025-26 / AY 2026-27

🟢 ITR-1 (SAHAJ)

Applicable For:

Resident Individuals having:

Salary/Pension Income

One House Property

Income from Other Sources (Interest, etc.)

Total Income up to ₹50 lakh

Not Applicable If:

❌ Capital Gains Income

❌ Foreign Assets or Foreign Income

❌ Multiple House Properties

❌ Business or Professional Income

Due Date:

📅 31 July 2026

🔵 ITR-2

Applicable For:

Individuals and HUFs having:

1. Capital Gains Income

2. Multiple House Properties

3. Foreign Income or Foreign Assets

4. Income exceeding ₹50 lakh

5. Director in a Company

6. Investment in Unlisted Shares

Suitable For:

✔️ Investors

✔️ High Net-Worth Individuals (HNIs)

✔️ NRIs (in many cases)

Due Date:

📅 31 July 2026

🟠 ITR-3

Applicable For:

Individuals and HUFs having:

1. Business Income

2. Professional Income

3. Freelancing Income

4. Consultancy Income

5. Proprietorship Business

Common Professionals Covered:

A. Chartered Accountants

B. Doctors

C. Lawyers

D. Architects

E. Consultants

F. Freelancers

Due Dates:

📅 31 August 2026 – Non-Audit Cases

📅 31 October 2026 – Audit Cases

🟣 ITR-4 (SUGAM)

Applicable For:

Resident Individuals, HUFs, and Firms (other than LLPs) opting for presumptive taxation under:

Section 44AD

Section 44ADA

Section 44AE

Conditions:

✔️ Total Income up to ₹50 lakh

✔️ Presumptive Income Scheme Opted

Due Dates:

📅 31 August 2026 – Non-Audit Cases

📅 31 October 2026 – Audit Cases

🟢 ITR-5

Applicable For:

Partnership Firms

1. LLPs

2. AOPs

3. BOIs

Due Dates:

📅 31 August 2026 – Non-Audit Cases

📅 31 October 2026 – Audit Cases

🔴 ITR-6

Applicable For:

Companies other than those claiming exemption under Section 11.

Commonly Filed By:

✔️ Private Limited Companies

✔️ Public Limited Companies

✔️ OPCs

Due Date:

📅 31 October 2026 (Audit Cases)

🔵 ITR-7

Applicable For:

Entities required to file returns under:

A. Trusts

B. Charitable Institutions

C. NGOs

D. Political Parties

E. Educational Institutions

F. Religious Institutions

Due Date:

📅 31 October 2026 (Audit Cases)

⏳ Other Important Income Tax Deadlines

📌 Transfer Pricing Cases

📅 30 November 2026

Applicable where transfer pricing provisions under domestic or international transactions are involved.

📌 Belated Return

📅 31 December 2026

If a taxpayer misses the original due date, a belated return may still be filed before this date subject to late fees and other consequences.

📌 Revised Return

📅 31 March 2027

Taxpayers can revise their already filed return to correct mistakes or omissions before this date.

⚖️ Consequences of Late Filing of ITR

Failure to file the Income Tax Return within the prescribed due date may lead to:

❌ Late filing fees under Section 234F

❌ Interest under Sections 234A/B/C

❌ Loss of carry forward of certain losses

❌ Delay in refunds

❌ Increased scrutiny risk

❌ Penalty notices from the department

✅ Benefits of Timely ITR Filing

✔️ Faster processing of refunds

✔️ Easy loan and visa approvals

✔️ Carry forward of losses

✔️ Better financial documentation

✔️ Compliance with legal requirements

✔️ Avoidance of notices and penalties

📚 Key Legal Provisions

Relevant to ITR Filing

Section 139(1) – Mandatory Filing of Return

Section 139(4) – Belated Return

Section 139(5) – Revised Return

Section 44AD – Presumptive Taxation for Businesses

Section 44ADA – Presumptive Taxation for Professionals

Section 44AE – Presumptive Taxation for Transporters

Section 234F – Late Filing Fees

📝 Final Thoughts

Choosing the correct ITR form and filing the return within the prescribed timeline is essential for smooth tax compliance. Taxpayers should carefully evaluate their sources of income, audit applicability, and disclosure requirements before filing the return.

With increasing data analytics and automated scrutiny by the Income Tax Department, accurate and timely filing has become more important than ever.

If you are unsure about the correct ITR form applicable to your case, professional guidance can help avoid future litigation, notices, and penalties.