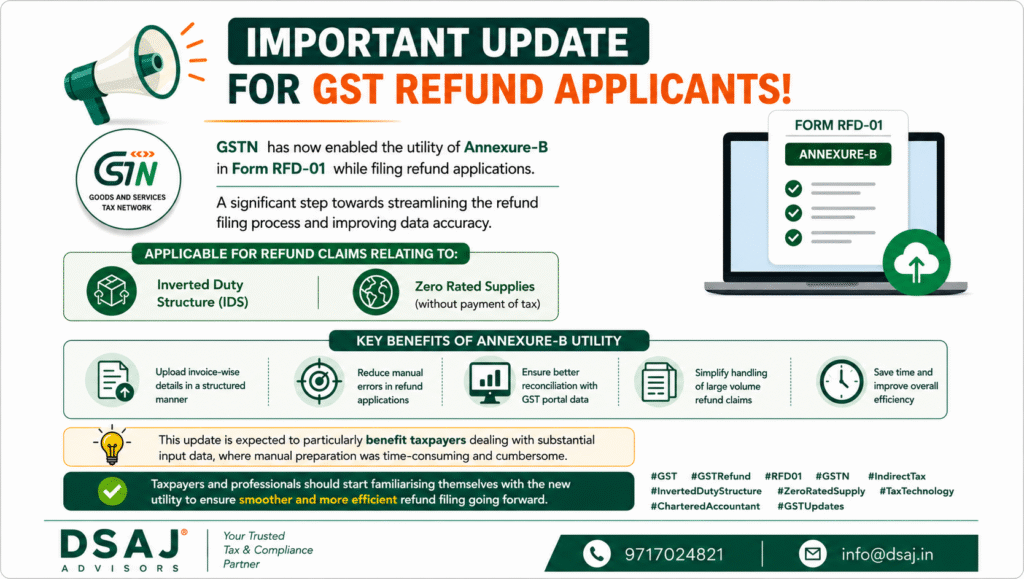

The Goods and Services Tax Network (GSTN) has rolled out an important system enhancement by enabling the Annexure-B utility in Form RFD-01 for specific refund categories.

This update is aimed at improving data accuracy, standardisation, and ease of filing GST refund applications, particularly for taxpayers dealing with large volumes of invoice data.

📌 Legal & Procedural Background

Refund applications under GST are filed in Form RFD-01 in accordance with Section 54 of the CGST Act, 2017 read with Rule 89 of the CGST Rules, 2017.

In certain refund categories—especially those involving input tax credit accumulation or zero-rated supplies—taxpayers are required to furnish invoice-level details to substantiate their claims.

Traditionally, this data was prepared manually or through offline utilities, leading to:

A. Increased risk of data inconsistencies

B. Errors in invoice reporting

C. Delays due to mismatches with GST portal records

✅ What Has Changed?

GSTN has now introduced a system-enabled Annexure-B utility within Form RFD-01, allowing taxpayers to upload structured invoice-wise details directly on the portal.

This marks a shift from largely manual preparation to a more digitised and standardised reporting mechanism.

📊 Applicability of Annexure-B Utility

As per the current rollout, the Annexure-B utility is available for refund claims relating to:

✔️ Refund under Inverted Duty Structure (IDS)

(Accumulation of ITC due to higher tax on inputs than output supplies)

✔️ Refund of unutilised ITC on Zero Rated Supplies without payment of tax

(Exports under LUT/Bond)

🔍 Key Functional Improvements

1. Structured Invoice-Level Upload

The utility enables taxpayers to furnish invoice-wise data in a predefined schema, ensuring uniformity in reporting.

2. System-Based Validation

Data uploaded through Annexure-B is expected to align more closely with GST returns (GSTR-1, GSTR-3B, etc.), thereby reducing mismatches.

3. Reduction in Manual Intervention

Eliminates the need for extensive manual compilation, lowering the risk of clerical and typographical errors.

4. Improved Reconciliation

Facilitates better cross-verification with portal data, which may reduce issuance of deficiency memos and notices.

5. Scalability for Large Data Sets

Particularly beneficial for taxpayers handling high-volume transactions, such as exporters and manufacturers.

📈 Practical Implications

• This development is expected to:

1. Enhance accuracy of refund claims

2. Reduce processing delays caused by discrepancies

3. Improve overall efficiency in GST compliance

4. Support faster verification by tax authorities

• However, taxpayers should note that:

1. Accuracy of uploaded data remains the responsibility of the applicant

2. Proper reconciliation with books of accounts and filed returns is still essential

⚠️ Action Points for Taxpayers & Professionals

• To effectively implement this update:

✔️ Review the Annexure-B template/format before filing

✔️ Ensure invoice data consistency with GST returns

✔️ Perform pre-upload validation and reconciliation

✔️ Update internal systems/processes to align with structured reporting

✔️ Monitor GSTN updates for further enhancements or validations

🧾 Conclusion

The enablement of Annexure-B utility in Form RFD-01 is a procedural and technological improvement rather than a change in law. It reflects GSTN’s ongoing efforts to digitise compliance and reduce manual inefficiencies.

While the utility simplifies the process, taxpayers must continue to exercise due diligence in data accuracy and documentation to ensure smooth processing of refund claims.